The Euribor rate is set for its biggest monthly fall in 15 years, with the average mortgage rate falling to €919 a year.

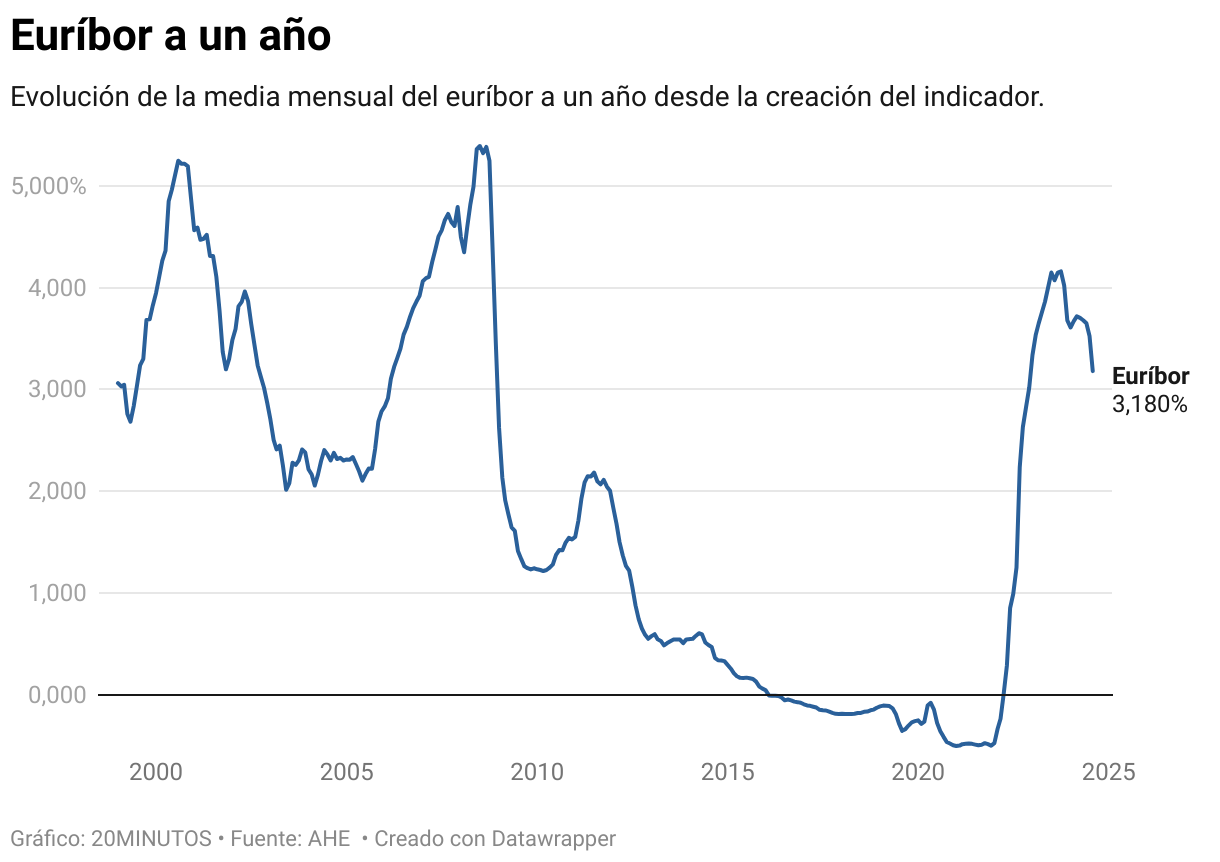

September is always a tough month for family finances, but this year it will bring a little relief to the pockets of those with a mortgage. Just four days before the end of August, the annual Euribor rate – the figure by which the installment plan for almost all variable-rate mortgages in Spain is calculated – On average, it is 3.180% per month.down 0.35 points from the July close, a rare crash that suggests significant changes in the monthly bills families pay.

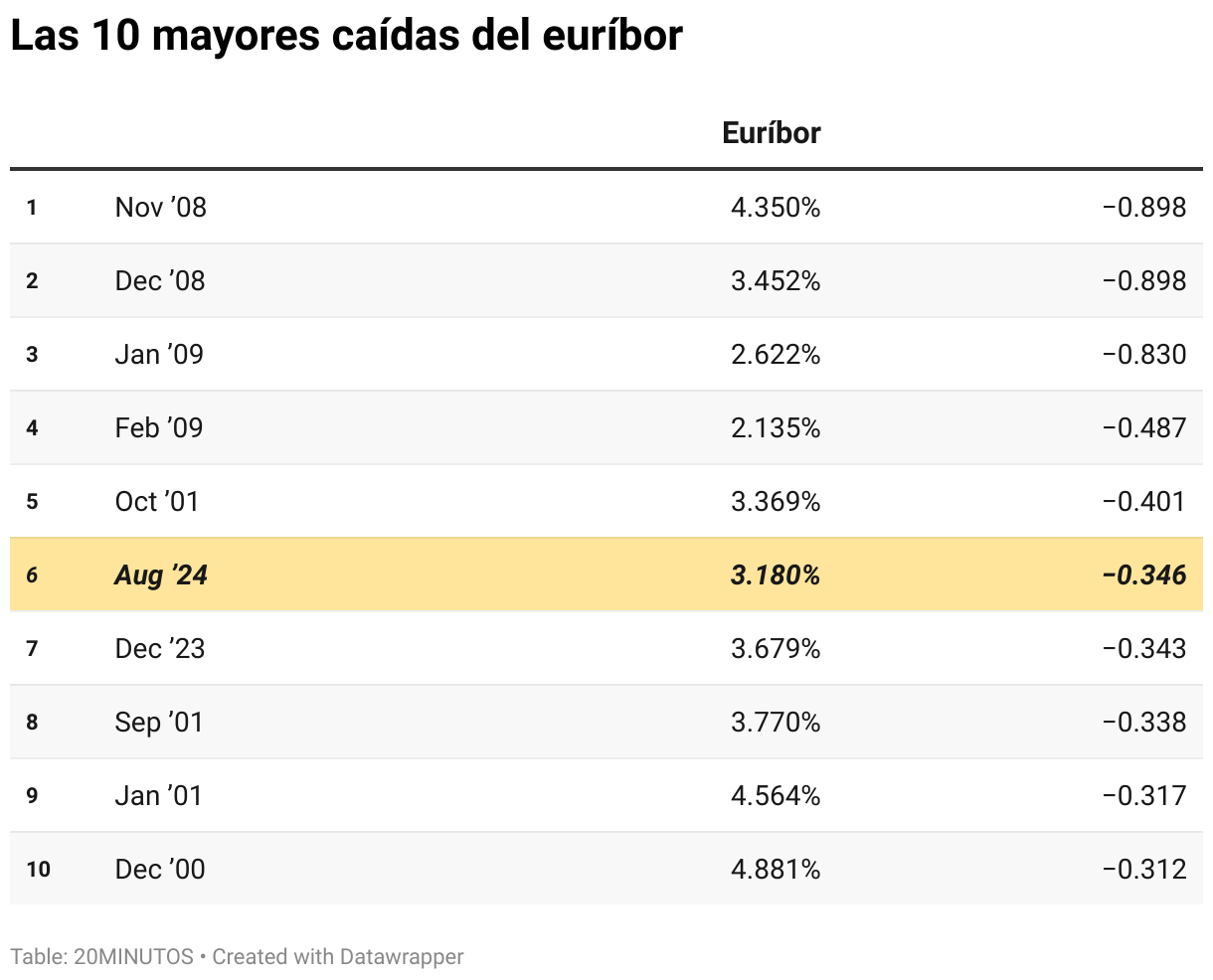

Barring disaster, Euribor will close in August. the lowest level since December 2022, the biggest month-on-month drop in the last 15 yearsTo find a similar collapse in just one month, you would have to go back to February 2009, at the height of the great financial crisis of 2008. We are facing the sixth largest fall in Euribor in the index’s history.which was introduced along with the euro 25 years ago.

The most tangible impact on families will be lightening your mortgage bill. An oxygen balloon that will be noteworthy in this case. For an average variable loan – 150,000 euros for 25 years with an annual review and a difference of one point compared to Euribor – which updates its contribution taking into account the August data. This could mean savings of up to €76.54 per month (€919 per year). For mortgages with higher debt, the relief will be even greater.

In any case, while the relief will be significant, the monthly bill that mortgage holders will pay will still be much higher than what they were paying before the inflation crisis. A scenario that does not look likely to return in either the short or medium term. According to preliminary data for August, Variable mortgages will still be 23% more expensive than they were in 2022. (which means €153 more per month for a typical loan like the one mentioned above) and 52% more expensive than three years ago, when Euribor was in negative territory.

Another derivative of the fall in Euribor that has been happening since March, although not as sharply as in August, is that the cost of new loans should become cheaper. The latest data published by the Bank of Spain shows that interest paid on new home purchases stood at 3.38% in June last year, almost six tenths below the peak reached in October last year.

Waiting for the ECB

lThe big question is whether this downward trend in Euribor will continue and for how long. The next clue on this issue will come from the European Central Bank (ECB) in just over two weeks. The institution that regulates the euro will decide on September 12 whether or not to implement a new cut in official interest rates – the rates that determine how much it costs to borrow money or remunerate deposits.

Markets are betting that the institution led by Christine Lagarde will vote to cut rates.. This view, according to ECB sources cited by Reuters, is shared by decision-makers at the central bank. The context seems favourable. In the eurozone, inflation remains stable at around 2.6% (very close to the 2% target); wage growth (a measure that worries the ECB greatly) has slowed, and the US Federal Reserve recently announced that it would cut rates for the first time in two and a half years after starting to raise them.

The signals central banks send in the coming weeks will be key to predicting the future of Euribor. This would not be the first time that markets have become optimistic and bet on a rate cut that ultimately does not happen.In December last year, Euribor already experienced a sharp fall similar to that in August, precisely because of the euphoria that eventually faded away.