Siemens Energy: artificial intelligence also plays in its favor | Financial markets

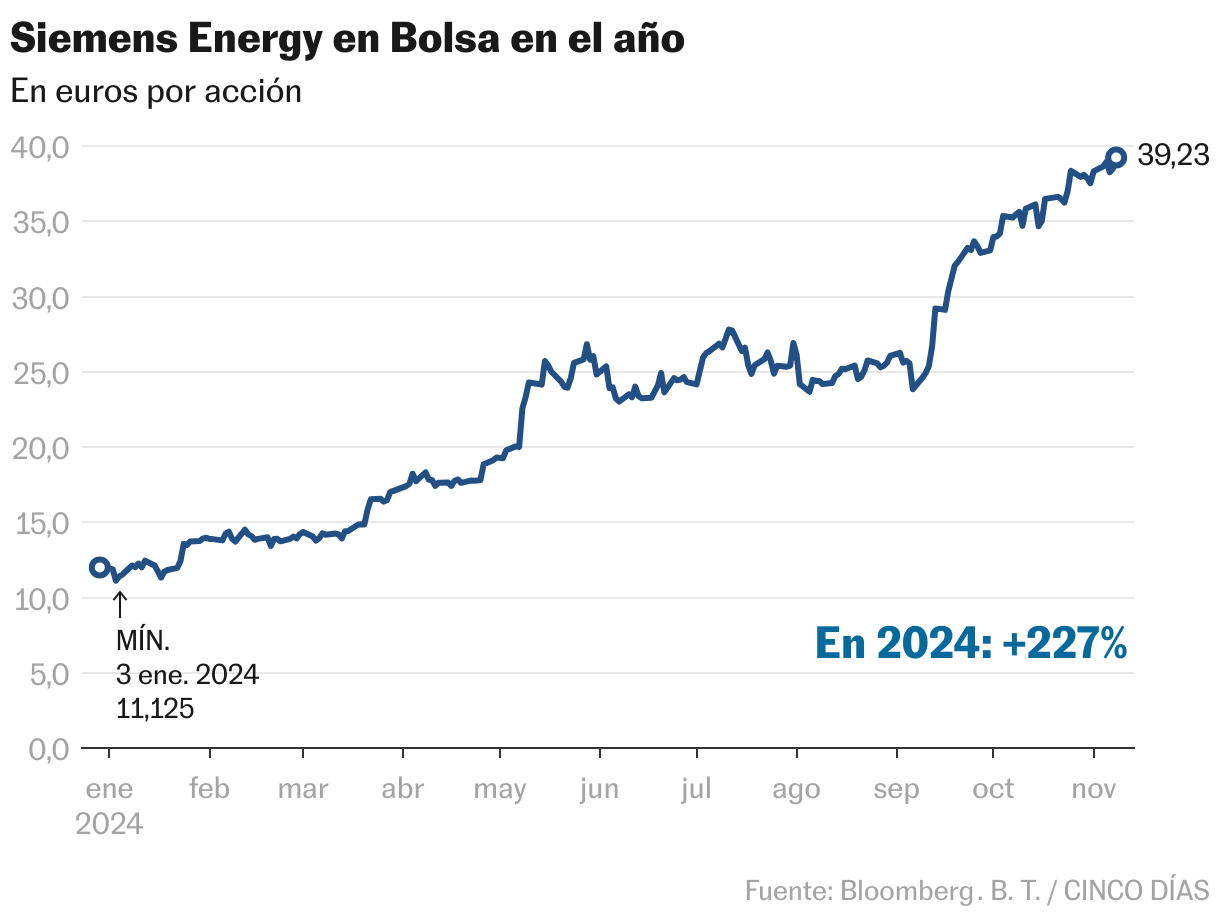

Siemens Energy has been on a downward spiral for some time now, and while Donald Trump’s victory has made renewable energy investors somewhat nervous about his critical stance on climate change, the company’s appeal to most analysts goes well beyond that. Over the year, he has gained 227% in the stock market and has 44% buy recommendations and 44% hold recommendations; the remaining 12% is for sale. The main controversy relates to the assessment achieved by the German. In fact, it has significantly exceeded the market consensus price target reported by Bloomberg at €35.2.

It is in the latest report from Deutsche Bank that analysts are trying to “make sense” of the situation in the stock market. “The perception of Siemens Energy is changing from a disruptive business due to the energy transition to a leader in electrification and decarbonization.” “The group is a global player in power generation and transmission and is well positioned to benefit from a multi-year supercycle of investment in electrification, which has recently received further impetus from data centers dedicated to artificial intelligence.” Having come to this conclusion, the bank positioned itself as one of the most optimistic and a few days ago raised its target price from 38 euros to 43 euros, an increase of 10%.

There have been more comments along these lines in recent weeks. Investors are starting to take notice that growing demand for electricity from data centers that power artificial intelligence applications is one of the main reasons companies are turning to natural gas generators like those made by Siemens Energy. Morgan Stanley also doesn’t view the company’s shares as expensive, based on its business outlook. “The consensus does not take into account the potential for profitability growth over the medium term in the gas and natural gas divisions. grid technologies given the favorable dynamics of supply and demand.”

For its part, Bank of America (BofA) focuses on differentiating the development of the parent company and the subsidiary. “Siemens Energy is a critical company in driving the world’s transition to sustainable energy through a combination of next-generation technologies.” However, at Siemens Gamesa, although the uncertainty of last year’s balance sheet has now been resolved, we are seeing a slow path to profitability.” “It is well positioned for growth in the offshore market, but there is deep uncertainty in the business. coastal“adds the firm.

Siemens Energy’s results for the first nine months of the 2024 financial year showed a profit of 1,588 million euros from a historical loss of 3,718 million in the same period the previous year due to serious problems in the wind turbine 5.X and the Siemens Gamesa 4 platform. X.

Barclays, on the other hand, has a radically opposite view of Siemens Energy, which it values at €21, well below current levels. He claims that his market advice is because “profits in gas and electricity They have improved, but are likely limited in their capabilities from now on; “Wind conditions will continue to be severe and have almost doubled in the last six months.”

In parallel, Morningstar states that “the stock is very overvalued and it has not completely ruled out uncertainty about its wind turbine business. The return to profitability depends on Siemens Gamesa’s recovery efforts and the magnitude of unexpected losses associated with the repair of faulty wind turbines.” For the firm, the fair value is €24.

Expecting a return to profit at the end of the financial year

Siemens Energy began a rally 12 months ago that has barely stopped. During this time, it grew by 263%, rising from an all-time low to a record. The company’s shares have weathered the period of uncertainty experienced by the renewable energy sector and are well past the crisis at its subsidiary Siemens Gamesa. With growth, it reached a capitalization of 31.3 billion. For its 2024 financial year results, which it will report on the 13th, Barclays expects total sales to be 34.743 million euros, compared with 34.484 million according to market consensus, representing growth of 11.6% and 11% respectively. The bank expects confirmation of a return to profit when losses exceeded 4.5 billion in 2023. For Morgan Stanley, this is the most important catalyst in the short term, and he also hopes that “they will announce mid-range targets.”