The ECB made two rate cuts for the first time since the euro crisis | Economy

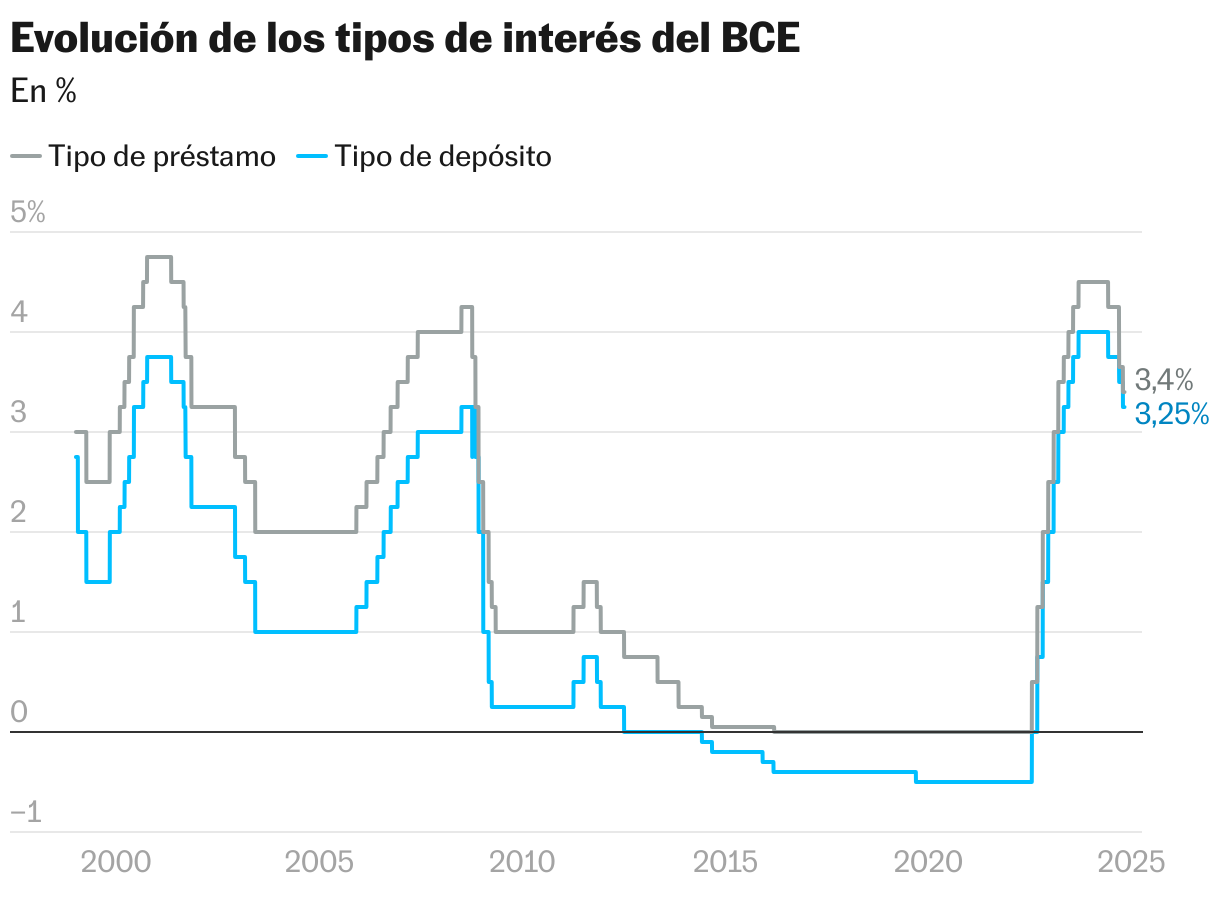

June, September, and now October. This Thursday, the European Central Bank announced its third interest rate cut in 2024, the second in a row, something that had not happened for 13 years when Mario Draghi, fresh from power, pulled out his arsenal to fight the euro crisis. Today’s, like the previous two, represents a small decline of 25 basis points, but enough to set a de-escalation trend in the price of money that already appears unstoppable in the coming months, given the good inflation data and poor growth. In its statement, the bank calls the latter a “recent surprise in the decline in economic activity,” a groundbreaking statement that clearly speaks to how concerns are gradually shifting from inflation to anemic growth among G20 countries. Following this move, the deposit rate stood at 3.25%, a level not seen in 16 months. All eyes are now on Education President Christine Lagarde’s speech, which will begin at 2:45 p.m.

This decision represents an attempt by the ECB to adapt. The European Bank has been repeating the mantra for months that it is not following a specific rate path, and reacts every meeting. That is, he avoids dogmatism and can change his mind if the data requires it. He delivered: a few weeks ago, the October meeting was expected to be one of those transitional meetings. Wait and watch without taking a single step. Reality, however, has pushed the Governing Council to hit the accelerator: inflation is already at 1.7%, the lowest level since April 2021, and below Frankfurt’s target of 2%. “The latest inflation information shows that the deflation process is continuing as expected,” says the bank, which presents wage growth as a risk at a “still high pace.” In parallel, eurozone growth is showing worrying signs: it was just three-tenths in the first quarter and two-tenths in the second, with no major improvements in sight. Both news together allow the ECB to think it is possible to continue removing the sandbagging that is slowing economic activity without implying overheating prices.

Even employment, one of the key factors in the economy’s resilience, is starting to show some cracks, with the vacancy rate, which measures the share of available jobs as a share of the total, falling in September. The situation is still far from alarming – unemployment remains at a historic low of 6.4% – but analysts say such signs should not be ignored. Or the same thing conveyed by industrial activity indices, which in September fell to their worst level in a year. The Franco-German axis, once the driving force of Europe, came into focus following the end of the Olympic movement in Paris and the threat of an imminent recession in Berlin.

The chronic nature of the military crises in Ukraine and the Middle East is not helping to restore optimism. Lists of potential risks are sometimes catastrophic, but others are absolutely right. In September, the ECB listed among the threats a possible increase in energy prices due to geopolitical tensions. And in October, those fears became reality: Iranian missiles flew over Israel and a barrel of crude oil became more expensive in the face of a hypothetical scenario of open war that would affect oil fields controlled by Tehran.

The storm, with obvious inflationary consequences, was in any case ephemeral. It appears to have died down as speculation about an Israeli attack that left Iran’s oil fields filled with plumes of black smoke has faded. But the storm remained a downpour, lacking both the duration and intensity to usher in a new era of barrel prices and derail the ECB’s plans to cut rates in October, although no one rules out the possibility of storm clouds coming. come back.

Lagarde too. His message at a dinner hosted this Wednesday evening in Ljubljana by the Slovenian central bank, host of the ECB meeting that once a year takes a breather from its usual headquarters in Frankfurt, was a demonstration of how the world is getting worse on fundamental issues. problems. “The global order we knew is fading. “Open trade is being replaced by fragmented trade, multilateral rules by state-subsidized competition, and stable geopolitics by conflict,” he warned.

This variable, as well as other structural problems ranging from falling German exports, weak industry, high energy prices and Chinese competition in sectors such as electric vehicles, are outside the ECB’s radius of influence. His ability to influence markets, make mortgages cheaper and more expensive, and raise and lower savings yields has given him a certain omnipotent aura that some decision-makers sometimes try to shake off. “Monetary policy is not a panacea,” recalled German Isabelle Schnabel, a member of the bank’s executive committee, this month.

In the part it controls, the ECB follows a clearer strategy among major central banks. Since the start of the summer’s rate easing, three cuts of 25 basis points across four meetings contrast with the Bank of England’s only cut of that amount in three meetings – following strong inflation data in September, which now stands at 1.7. %, the market expects a second one to arrive in November – and another from the US Federal Reserve in three meetings, albeit a more aggressive one, at 50 basis points. The record also represents a victory for the less orthodox sector, known as the doves, over the hawks, who offered little resistance.

The ECB’s last appointment this year will take place on December 12. If the ECB’s forecasts come true, the data up to this point will not be the best. “Inflation is expected to increase in the coming months and then decline to target over the next year,” the bank explained. Despite this, given the temporary nature of the price increase, the downward streak is expected to continue. Not just until then, but for a long time: Bank of America analysts are forecasting interest rate cuts of 25 basis points at each meeting until the interest rate returns to 2% in June 2025.

(Latest news. Update coming soon)