The Spanish bank will become the least capitalized in Europe in 2025 | Companies

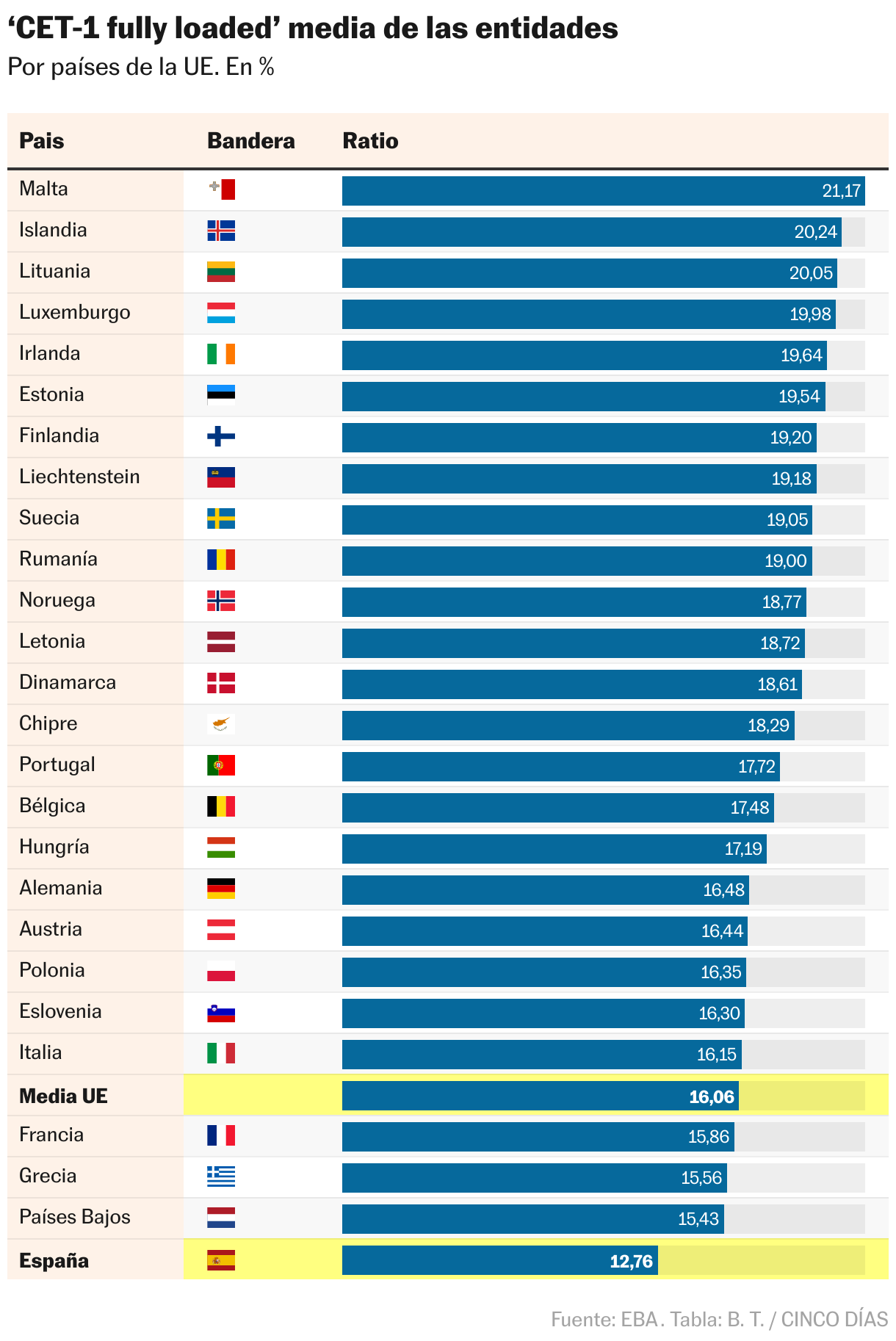

The Spanish bank ranks near the bottom of its capital stock compared to its European peers. National institutions report a CET ratio of 1 on average, according to data published this Friday by the European Banking Authority (EBA) following a 2024 transparency exercise in which it monitors the risks of the European financial system. fully loaded (which defines capital of the highest quality) of 12.76% compared to the EU average of 16.06%. Thus, businesses are approaching 2025, when new standards for calculating capital adequacy ratios will come into force due to the application of the new Basel III rules.

The rate presented by the Spanish institutions is in any case significantly higher than the requirements set by the European Central Bank (ECB), amounting to around 12%. In recent years, Spanish banks have consistently ranked last in the EU in terms of capital levels. However, this does not mean that its solvency is weaker than that of banks in other countries. The banking regulator determines minimum capital levels based on the risks of each organization and its business model. The lower this requirement, the less risk you have. Therefore, the requirements are different for each subject. The goal is to ensure that banks have enough of their own funds to cover potential losses.

Among Spanish enterprises, Kutxabank is again recognized as the most capitalized enterprise in Spain with a share of 18.21%. It is followed by Unicaja with 15.08%, then Cajamar (13.82%), Sabadell (13.47%), Ibercaya (13.2%) and Abanca (13%). One step behind are BBVA (12.75%), Santander (12.46%), Bankinter (12.44%) and CaixaBank (12.22%).

Likewise, delinquencies remain at historically low levels, below the 3.11% reported by BBVA. The best rate is from Kutxabank – 1.48%, as well as Ibercaja and Abanca – 2% each, as well as Bankinter (2.22%), Unicaja and Cajamar (2.5% in both cases). In terms of coverage level, CaixaBank is the best bank with 53.5%, followed by BBVA (49.4%) and Bankinter (48.6%).

Kutxabank in a press release emphasizes the bank’s leading position in terms of solvency, efficiency, leverage and default in the European sector, which allows it to be above the European average. “The strength of Kutxabank’s business model is also reflected in improved profitability, market risk, credit and sovereign risk, doubtful balance sheets and refinancing risks,” he points out.

The EBA report weighs in on rising geopolitical risks, although it notes limited exposure to the first round of these risks; not so for those in the second round. It also takes into account climate and physical risks, as well as rising operational risks, mainly related to cybercrime.

The institute, headed by Spaniard José Manuel Campa, describes the capital situation of European banks as stable, well above the minimum levels set by regulators. It takes into account the high profitability of businesses, although it cautions that these levels are unlikely to be sustainable in a falling interest rate environment. The company also acknowledges the jump in this figure compared to its European competitors.

ECB announces changes to the Eurosystem framework

The Governing Council of the European Central Bank (ECB) today decided to take action to promote harmonization, flexibility and efficiency in collateral risk management. Since the global financial crisis, the Eurosystem has operated two collateral systems: a general structure, which is permanent, and a temporary structure, in which measures have been applied to relax the criteria for the admission of collateral-linked assets in times of crisis. The adjustments agreed today aim to return to a single, agreed list of collateral assets available to all counterparties, regardless of their location in the eurozone. The Governing Council decided to incorporate some measures from the temporary framework into the overall framework. Likewise, the Governing Council agreed to continue the phasing out of temporary measures to ease the admission criteria for crisis-related collateral.