Wars in Ukraine and Gaza have sharply increased the value of major arms companies | Economy

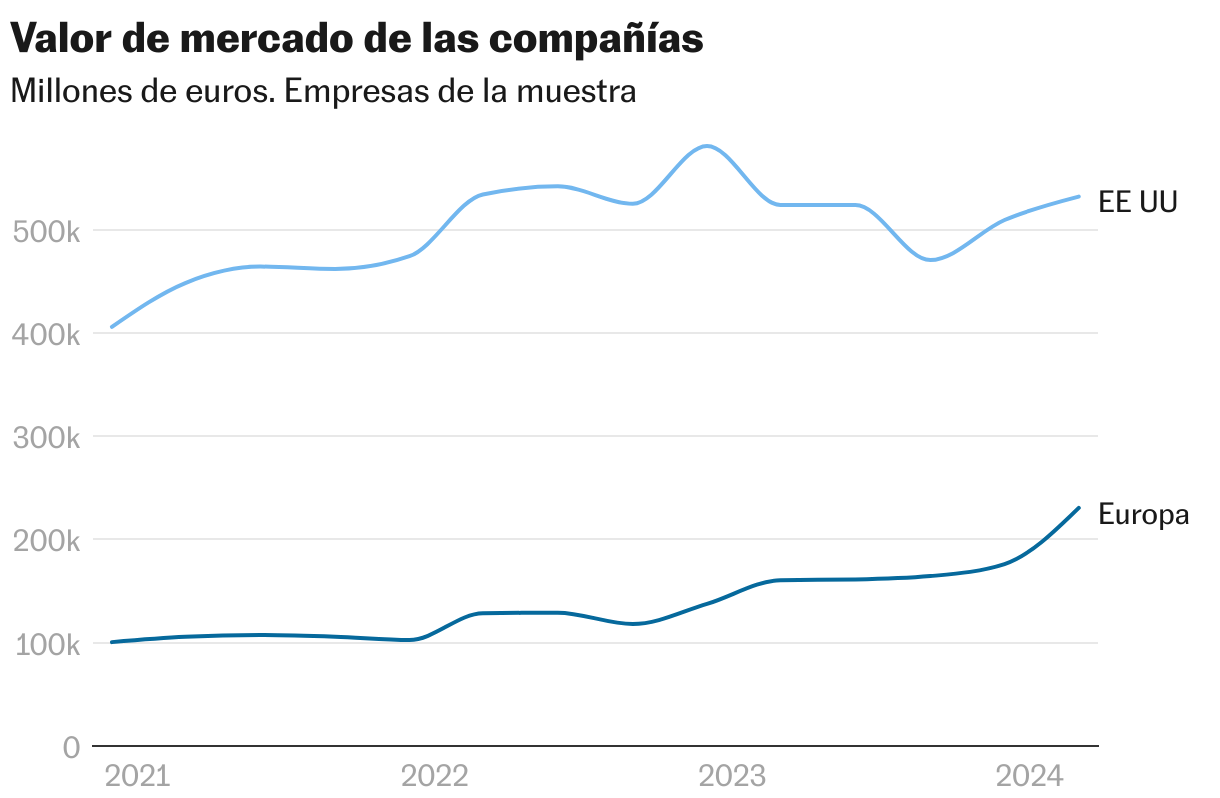

The market value of the main companies producing military equipment in the US and Europe has soared over the past two and a half years under the cover of the wars in Ukraine and the Gaza Strip. This is confirmed by a study by the consulting company Accuracy, which analyzed the evolution of seven major US companies in the sector and their peers on the Old Continent, whose stock market capitalization has grown by 59.7% since February 24, 2022, when the invasion of Ukraine began. The growth is much higher than that of the main stock indices on both sides of the Atlantic (S&P 500 and Eurostoxx 50), which have recorded growth of just over 13% and 7%, respectively, over the same period.

The US companies analysed included Honeywell International, RTX Corporation, Lockheed Martin, Northrop Grumman, General Dynamics, L3Harris and Huntington Ingalls. On the European side, they included France’s Safran, Dassault Aviation and Thales; Britain’s BAE Systems; Germany’s Rheinmetall; Italy’s Leonardo; and Norway’s Kongsberg Gruppen. Ignacio Liiso, a partner at financial and strategic consultancy Accuracy, explains that the companies selected were large ones in which the defence sector has an appropriate weighting.

While the study covers the period from January 2021 to March of this year, its biggest price gains occurred between the third quarter of 2023 (when Israel’s offensive on Gaza began) and the first quarter of 2024. The 14 arms industry giants rose by 20%, it notes. “In the week following the Hamas attack on October 7, the average share price of the companies in the sample rose by about 9%, while the (stock) market remained stable,” the report, compiled from the Capital IQ database, says.

The increase in the company’s market value led to its EBITDA (annual earnings before interest, taxes, depreciation and amortization) growing from 11.1 times to 18.8 times, or 68.4% more.

But it wasn’t just the price of its shares that soared, but also the volume of securities traded. In the first quarter of 2022, coinciding with the invasion of Ukraine, investors sold shares of European companies worth €1,402 million, the highest amount in the last eight quarters; while the traded securities of American companies reached their record (€1,034 million) in the fourth quarter of 2023, coinciding with the escalation of violence in the Middle East.

The growth in the prices of European companies in this sector was stronger than that of their North American peers (129% compared to 31%), which Llisso explains by the fact that the growth in the US “started earlier, and the European stock markets then joined in”. Despite this, the difference between the two groups remains daunting: the market value of the seven American giants reaches 532 billion euros, while the market value of their European peers remains at 230,583, i.e. less than half.

The profitability of the military industry has not grown at the speed of its stock market value, since the latter is a derivative of the expectation of future profits, and the materialization of contracts can last for a long time. “When the war in Ukraine begins, we see that the distance between the relative valuation of companies and their results increases: shares rise, and the turnover level remains the same. The investor is looking not only for immediate profit, but also in the medium term,” explains the Accuracy partner.

The average EBITDA margin of the two groups (American and European arms companies) remained stable during this period, fluctuating between 14.3% at the end of 2021 and 12.7% at the beginning of 2024, although one on this side of the Atlantic increased by 2.1 points (from 11.7 to 13.8%), while the other decreased by 4.3 (from 16.5 to 12.2%), narrowing the gap between them.

The most profitable

The American company Honeywell, which specializes in electronics and communications, has shown the greatest profitability, with an average of 24.2% over the period. On the other hand, the German company Rheinmetall, a manufacturer of weapons and ammunition, has increased in value the most: its shares have risen from 96.7 euros in February 2022 to 334 in January of this year. That is, they are worth 245% more. “They all benefit from the (military) situation, although some, due to the type of products they invoice, do so more directly,” explains Llisso.

Leonardo’s stock price rose 139%; BAE Systems’ 101%; Dassault Aviation’s 86%; Thales’ 76%; Konsberg Gruppen’s 64%; and Safran’s 45%. American companies’ stock price gains were somewhat more modest: Huntington Ingalls’ 40%; Lockheed Martin’s 29%; General Dynamics’ 25%; and Northrop Grumman’s 22%.

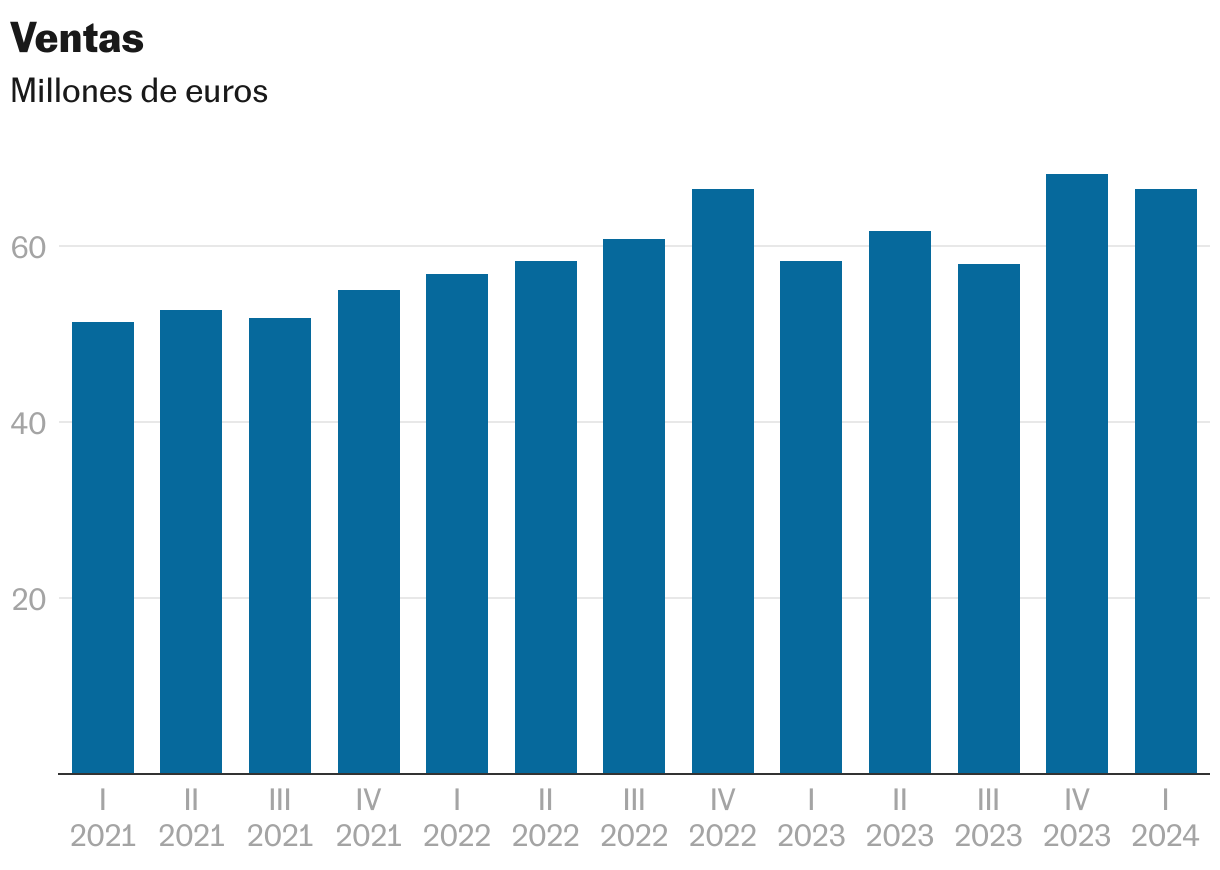

In terms of invoicing, the sales of US companies increased by 27.47% (14,122 million euros) when comparing the first quarter of 2021 with the first quarter of 2024, while the sales of European companies increased by 28.82% (6,828 million euros) in the last quarter of 2024 (there is no complete data for the first quarter of this year) and the last quarter of 2021. In any case, these are not comparable volumes, since last year the turnover of seven US companies increased by 246.157 million euros, while European companies registered 102.327 million, 41.5% of them.

Even when the wars in Ukraine and Gaza end, markets are betting on a long period of rising military spending, with most NATO countries already spending more than 2% of GDP on defense and the rest of the world entering a new arms race. “There is a very strong inflow of capital into the defense sector,” says Llisso. Between guns and butter, investors are in the clear.

Keep up to date with all the information Economy And Business V Facebook And Xor in ours weekly newsletter